Steve's blog about RMPrepUSB, Easy2Boot, USB booting, Investing and sometimes other stuff too!

Visit www.rmprepusb.com for over 140 Tutorials on USB booting or www.easy2boot.xyz for a unique USB multiboot solution.

What is a 'safe' and simple investment stock portfolio for family and friends?

I am often asked by family and friends what they should invest in. This is an extremely difficult question because I don't want to be disowned by them if they lose their money!

Stock and Shares investment is a long term commitment.

They can go up-diddly-up-up or down-diddly-down-down!

Be prepared - in some years your investment pot may decrease a lot in value but don't sell!

If you can't stand to see your portfolio lose 20% in a year, then you could choose a nice safe savings account instead! However, savings accounts barely keep up with inflation. If you are a high rate tax payer and put £100K into a savings account paying 5%, then in the UK each year you will pay 40% of that 5K interest to the tax man! If cashing out after 5 years, due to loss of compounding and the tax difference, you will be about £5K better off with a 5% gain ETF even if in a taxable S&S account, than in a 5% savings account.

When investing in Stocks and Shares we must consider:

Is an income required (Accumulating or Dividend portfolio)?

Tax laws in your country of residence and using them to your best advantage

Attitude to risk and loss (would you mind if your portfolio went down 40% in a year?)

Do you need access to the money within a few years - e.g. to buy a house or car?

As I live in the UK, I will mainly discuss the stocks available in the UK, but similar alternatives in other countries are usually available and the USA has a much wider collection of funds available than we do in the UK, e.g. many more Vanguard funds and other ETFs such as SCHD and VOO.

I will choose the example of growth investing with a fund of £100,000 for the sake of simplicity (accumulating fund), but most investors will simply want to build up their investments by adding into their investment account each month. This is best done by setting up an automatic payment from your bank account just after your monthly pay day, so that you don't forget to invest!

Trading 212 will allow you to set up a portfolio as a 'Pie', and then you can invest monthly into the Pie and that payment will be used to buy more ETFs in the proportion that you chose previously.

UK investors have access to a tax free account called an ISA in which they can deposit a maximum of £20K a year. Even better tax advantages can be had by investing into a SIPP Pension account.

I will not consider tax in this article much, except to say that for UK tax payers, you should really look into Flexible ISAs and SIPPs! If you are a high rate tax payer in the UK, your savings gains will be taxed 40% every year, if they are not inside a tax free investment account! However, if they are inside an ISA, for instance, you will pay no tax, but even if your are investing within a General Investment Account (GIA) you pay tax only if and when you sell your stocks and even then you will pay 24% rather than 40% tax.

Core + Satellite

Most investors will have a large part of their portfolio in just one or two shares (called the 'core'). These stocks are hardly ever sold and they will thus build up over many years and beat inflation. Investors then have a few more satellite stocks which may be more volatile and which they may change (sell) from year to year. I will consider a simple example, but you can have a wide variety of satellite ETFs (but the more you have, the more your gains will be diluted).

Core ETFs

Note that even a core pot will decrease in value in some years - e.g. in 2020 when we had Covid 19, or the 10% market dip in 2022. The idea is that over many years (5+ years) your core holdings will always increase at a faster rate than inflation.

A typical core holding would be an All-World or Global ETF (for non-USA investors).

I recommend HMWO for this because it has a lower charge (TER) than the benchmark standard SWDA. HMWS is the accumulation version which does not pay out the small dividend but just adds it back in.

Although a Global Index tracker like HMWO has about 20% of the portfolio in the 'magnificent seven', it also has shares in over 1000 other companies and so is quite widely diversified with 30% of stocks in non-USA companies.

It is a widely held conviction that one of the best investments you could make is to simply invest in the top 500 USA companies - the S&P500.

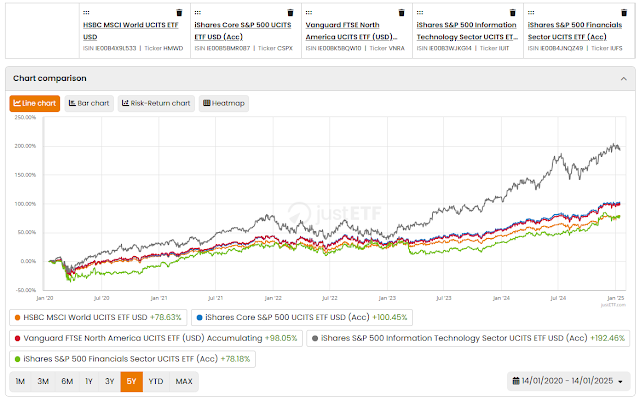

Whereas the ETF HMWO has returned 78% gain in the last 5 years,

the S&P500 has returned 100% (i.e. the S&P500 has doubled in five years).

However, if investing now, instead of going for a good S&P500 fund like CSPX for instance, I would plump for the North America ETF from Vanguard VNRA. This holds 570 stocks as opposed to the 500 in CSPX and is not quite so top heavy in the Magnificent 7 as the S&P500 is.

So for a diverse, low-risk core we have HMWO and VNRA. There is quite a lot of overlap between these two ETFs, but it does not matter because the overlap will be in good, large companies. Depending on your risk appetite, you can vary the weighting. If you want to be a steady investor then perhaps choose 60% HMWO + 40% VNRA as your core.

If you live in the USA, you might want to opt for a much higher weighting of VNRA than the All-World tracker ETF HMWO.

Generally, an actively managed fund will NOT consistently outperform a tracker ETF. One exception seems to be the excellent UK fund Royal London Global Equity Select. This has beaten the HMWO over 6 months, 1,3,5 and 10 years. However, since this is actively managed, it is highly dependent upon the skill and dedication of it's managers, and those managers can change over time. This fund is also not as easy to trade as an ETF and must it be done via a broker such as Interactive Investor or Barclays (not currently available from Trading 212 or Invest Engine).

Royal London gained 150% in 5 years (HMWO gained 81% in last 5 years)

Satellite stocks

Next we can pick some stocks which may be more volatile but may show even better returns than your core ETFs.

Satellite ETFs can be chosen by value, growth, commodity, sector or some other factor. They are typically higher risk and more volatile, but will hopefully give better gains than a diverse ETF like a global or North America ETF.

My favourite is the Tech stocks that are within the S&P500, these are held inside the ETF IITU.

IITU has returned almost a 200% gain in the last five years and around 40% in the last year.

XLKQ is a variation on IITU which limits exposure to any one company to 20% and has performed even better than IITU. One simple Satellite portfolio would be 70% HMWS+30% XLKQ for Global ETF + US Tech ETF.

HMWS is the accumulating version of HMWO

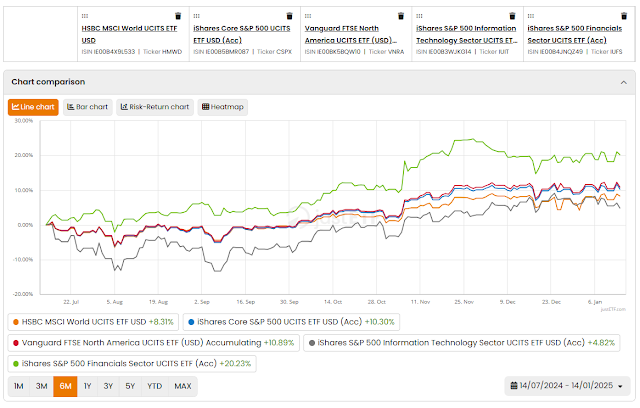

There are many more ETFs you could add (e.g. IUCM communication sector ETF), but another favourite of mine at the moment is the Financial sector ETF IUFS.

IUFS (green) in last 6 months

IUFS has outperformed all of the above ETFs in the last 6 months by a factor of x2.

Governments are recovering after the expenditure on Covid 19 and they will be raising capital via Gilts and Bonds which all go through the banks. Interest rates are high but they are slowly falling and the stocks and shares market is uncertain at this time. Public borrowing (debt) will increase. This means banks and financial institutions will take advantage of a high credit economy.

IUFS should not be seen as a long term holding however, and you should always review your satellite holdings at least once a year.

Simple Portfolio for 2025

So if starting a new portfolio in 2025, I would suggest a mix something like this:

HMWO or HMWS 30%

VNRA or VNRG 30%

IITU or XLKQ 30%

IUFS 10%

10% is about the minimum proportion I would have for any ETF because holding less than that will make little difference to your overall performance even if it doubled in a single year. You could split the 30% IITU and hold 15% each of IITU and IUCM. Another option is to also add the Utilities sector (10% IUSU + 10% IITU + 10% IUCM).

e.g. a 100K portfolio contains 5% of Acme Rocket Labs Plc. In one year it gains 50% in value (highly unlikely!), so you have made 2.5K in one year - whoopee! However, 60% of that 100K is in your core holdings which gained 25% in that same year (60Kx0.25=15K). So has taking that extra risk really made much difference? Whereas, if that risky Acme Rockets instead lost 50% in value, it will take you 2-3 years to get that loss back.

For investors, losses act like poison!

'Slow and Steady' large ETFs may be boring, but in the long term (10+ years), it is the best way to invest (even if not as much fun).

Emergency funds

Most investors like to keep an Emergency pot of cash in case of major events such as needing a new car, sickness or job loss.

UK tax payers can make use of cash ISAs if they wish and get a steady rate of return with no risk or tax to pay (e.g. approx. 4%) out of your 100K pot, you could keep £10K-£20K in a cash ISA. If it is a flexible ISA, you should aim to replace any withdrawn cash by April if possible, to avoid losing the tax free benefit on that account (£20K deposits tax free each year). Trading 212 currently pays 4.9% on all savings (even outside an ISA).

A UK higher rate tax payer will pay 40% on savings interest. If your ISA is full, then an alternative is to buy a money market fund such as CSH2 (check current interest rate - currently CSH2 pays just under 5%/yr variable). Capital Gains Tax (CGT) is only payable if and when you sell this ETF (18% or 24% if you are a higher rate tax payer) and you won't pay 40% (high rate tax) every year like you would if it was in a savings account. Note that there is a small extra cost when buying the CSH2 ETF, so it should not be used for short terms of less than a month or so and there may be an income component which is taxable (ERI) as well as a capital gain on sale.

ETFs discussed in this article:

5 year performance chart

Note that HMWO pays a small quarterly dividend of under 2% a year. 1.5% of £30K = £450/yr.

UK investors have a £500 tax free allowance, so no tax will be due on dividends under £500/year.

HMWS is the alternative that does not pay a dividend (accumulation version).

Research

There are lots of videos on You Tube about investing (do NOT watch any stock tip videos!).

Check what tax exempt savings, pensions and investment vehicles are available in your country.

If in doubt, pay an Independent Financial Advisor (IFA) or a registered Wealth Manager to help you (do NOT use an advisor that is connected with a bank or other finance company).

Note that IFAs will never advise you to self-manage your own investments because they could lose their licence for giving bad advice if you then lose a lot of your money by following that advice - they always play safe!

A recent investment video is shown above (note: Emerging Markets have hardly ever outperformed a global index or S&P 500 - no idea why one would invest in such a market!).

Please also see my blog article on my favourite ETFs and my 2 ETF world portfolio which beats the S&P 500!

No comments:

Post a Comment