Steve's blog about RMPrepUSB, Easy2Boot, USB booting, Investing and sometimes other stuff too!

Visit www.rmprepusb.com for over 140 Tutorials on USB booting or www.easy2boot.xyz for a unique USB multiboot solution.

This article mainly applies to UK residents but the general principle applies to most countries.

WARNING: If you have a non-state Pension, you may be being ripped off!

Reading this article can save you a lot of money! Someone may have robbed you of at least 20K and you don't even know it!

Pensions

A Pension is basically just a tax-efficient investment wrapper. So it usually is a way to get free money from the government as well as saving money. Pension companies invest money in the stock market (and maybe a proportion in bonds). Some stocks can lose money every year, some gain each year but at a lower rate than inflation (after costs) and some can gain over 20% a year.

These days, many sensible people, especially if self-employed, will invest in a personal (non-state) pension.

A pension company will take your money (or part of your wages), invest it, charge you for giving them your money and then give you back whatever is left in the pot when you retire. They don't care if it has gained 1000% or lost 50%, they still take their annual commission. If you are lucky they will tell you each year how big your 'pot' is. If you are even luckier, they will tell you the %age gain/loss you made that year. If you are very, very, very lucky, they will even compare their performance against other pension and stock market benchmarks ('oh look - there's a flying pig'!) - the regulations say they are supposed to state their performance (but curiously NOT in the annual statement they send to you!) - so you may have trouble in finding it! You are even luckier still if, each year, they actually tweak your portfolio that they have bought with your money, to get you the most they possibly can for you (oh yeah, that will never happen!).

Let us take an example:

You contribute £40 a month into a SIPP or other pension scheme. The UK government will add 25% (£10) to top this up to £50. So after 20 years, you will have accumulated 20 * 50 * 12 = £12K.

However, because the pension company has invested it for you, you should have a much bigger pot than 12K when you retire.

There are two very important things you MUST ask about your pension:

1. What was it's performance in past years and what is it's expected performance in future years (expressed as a percentage gain or loss per year).

2. What (hidden) charges are made by the pension company and the funds they invest in. This can add up to well over 2% of the total amount in your pension every year!

Now you pension company usually do not want to tell you the answer to either of these two questions and they often hide/bury/disguise/manipulate the answers very effectively on their website and in their literature.

However, you need to study the numbers that the pension companies actually report as they often do not show other charges which have a drastic effect the real performance. For instance in a report provided by Aviva, they quote a 2023 'gross' gain of 8%, but other sources (which includes all charges) show the real net figure for the same fund at only 4%. Aviva's own Pension Calculator on their website assumes a net annual gain of 2.9% - that should tell you something!

Also, many pension funds actually lose money in some years. This is not unusual when investing in the stock market, but a loss of say 5% in 2022 followed by a gain of 5% in 2023 means you have still lost over 2 years (not even accounting for inflation)!

Annual gain calculation

Putting the sum of £40 each month into your pension (UK Gov adds 25% = £50 a month = 12K), how much would your pension pot reach after 20 years (approx)?

4% annual gain = 18.5K (typical pension performance - though Aviva suggest 2.9%)

7.5% annual gain = 28K

8% annual gain = 29.7K

9% annual gain = 33.7K

10% annual gain = 38K (typical global market performance)

15% annual gain = 75.8K (actual SWDA gain averaged over 5 years)

Note that an average annual gain of global shares on the stock market has averaged well above 8% in the last 10 years! Note what a whopping difference there is between 4% and 10%.

SWDA (a global index tracker ETF) in last 5 years has averaged 15%, so which do you prefer (Aviva LifeStrategy 4% = 18.5K after 20 years, or the SWDA ETF 15% = 75.8K after 20 years - that's a difference of 57K that goes into your pocket and not into Aviva's pockets!).

Barclays 5yr performance averages: Multi-asset funds ranged from 4-6%. The Best Barclays pension was 'Barclays Global Markets 5' = 9% (only 10% in bonds - labelled as high risk to put you off!). Compare with SWDA at 15% average annual gain!

If you extend the pay-in period to 30 years instead of 20 years, you would have 350K (and in practise you would increase the £40 contribution over time too - a 2% increase each year on the initial £40 a monthly payments would give you a pot of 400k when you retire in 30 years)!

These are not pie-in-the-sky figures. This is based on past data (but does not take into account the cost of whatever your platform/broker charges you for your pension account - this can be as little as 0.15% a year with InvestEngine for instance). SIPP and UK broker advice here. Tip: Don't base your choice solely on who has the lowest fees as any broker can raise their fees at any time, instead look for a well established, reputable broker who will support you and still be in business for the next 30+ years.

Just who was your original pension advisor?

Before you stop reading this article because you had professional advice from a pension advisor (bank, pension company, etc.), just stop and think a minute. What was the motivation behind his/her advice and their pension recommendations to you?

Your motivation:

1. I want to get the most amount from my pension

His/her motivation (assuming not a truly independent Financial Advisor):

1. I want to get the most commission I can from this customer without them realising it

Now he/she has a range of pension products, but some schemes pay a LOT more commission than others. Which one do you think they are going to suggest? The current regulations are a lot stricter (not allowed to charge a %age-based commission), but when you took out your pension, they were probably not strict at all and your advisor would have been paid a fat commission (this could have been 5% of the payments you made for the first 5 years, for instance).

Even Independent Financial Advisors (the best sort) often have commission arrangements with some companies (did they 'help' you with the paperwork/sign-up process)? I am sure it did not affect their recommendations though ;-). IFAs also tend to be super-cautious with their advice and will follow industry guidelines because if they suggest a self-invested SIPP for instance and you complained that you lost money through bad advice, they could be severely penalised. They have to play it safe. It's like the old adage 'No one ever got fired for buying IBM'.

Even if your IFA gave you good unbiased advice, will they ring you if/when the market changes (e.g. USA stocks start to underperform or Japan or EU or UK stocks start to outperform)? Will they say 'hey Joe, I don't think your pension scheme will perform so well in the next year' and will they help you rebalance your portfolio or change your pension scheme? Is rebalancing your portfolio even possible as the stocks are held within funds and a large pension company is not going to change them! Even if they wanted to change the stocks that they hold, it is very difficult for them because as soon as they start to sell millions of £ of a stock or fund, the price of that stock/fund will plummet and they will get even less for it. Whereas, if you controlled your own self-invested pension, you could quickly adjust your ETFs yourself.

I strongly suggest that you now read these two Martin Lewis' articles:

Most people will ask a professional for pension advice because they themselves do not understand pensions. They assume they are paying a pension company for their expertise. A pension/financial advisor will give the excuse that they never suggest a self-managed pension to clients as you could be a complete idiot, lose money and blame them. What they don't tell you is how ridiculously easy it is manage your pension yourself and how you can easily double the performance of their pensions!

Pension companies, banks, financial institutions, etc. all employ sales people, office staff, hire buildings, etc. They are usually highly paid and have suits and expensive cars, but who do you think is paying for this? That 20K difference in your final pension pot (see above) is paying their wages and bonuses!

Many employers will automatically enroll you into a pension scheme. The employer will naturally choose the pension company that offers their services for free (e.g. Nest). So how does that pension company make any money? Well, from you obviously! They auto-enroll you in their 'default' pension scheme and charge you for giving them your money for 40 years. Just investing in a bog standard world tracker ETF has returned over 8% on average, pension companies typically return less than 4% - where do you think the other 4% of your money goes? Yep, into their pockets! So find out NOW about your employee pensions and how they have performed (even with your employers contribution).

But it gets worse. Let us say you contact your pension provider (maybe online) and switch your current pension scheme over to one of their more 'risky' pensions or even a self-investment pension. These let you choose from a range of funds, so you now can choose anything you like - right? WRONG. They may only allow you to choose from a very small selection of their own funds - not the whole world market and cheaper funds. Needless to say, their own funds don't seem to perform well when compared against other publicly available funds and their hidden charges seem to be very high too.

Many pension companies, including Aviva, allow you to transfer your pension to a SIPP and self-invest in ETFs. They usually make a small annual management charge (e.g. 0.4%) as well as trading costs and the (hidden) ETF OCF costs however.

Most pension funds would massively out-perform if they simply invested in a two-part mix of bonds + a Global Index tracker ETF like SWDA. So why don't they do it instead of investing your money in dozens of expensive funds and then charge you commission and other hidden charges? Why do they invest 40% of your money in bonds at age 30 when you cannot draw on it until you reach 57?

We are talking about £100K or more difference here when you retire!

Instead, you could have a self-invested SIPP and manage it yourself according to your own risk preferences which may change with time. e.g. a simple plan might be:

Age SWDA/Bonds ratio

20-30 90/10 - mostly invested in global stocks (many people are 100% in ETFs)

40 80/20 - 20% in bonds (depending on your circumstances - can still be 100% in ETFs)

50 70/30 - 30% in bonds as near retirement and stock market may dip for a few years

now nearing retirement age - consult a good independent financial advisor

60 60/40 - 40% in bonds (calculate how long you can draw down at this rate - adjust bond ratio) or follow FA advice.

But self-investing is risky, isn't it?

What pension companies tend to do is invest your pension money (which you and the UK gov have given to them) into a LOT of different funds. These funds can have high charges typically (over 1%) and may also pay a fraction of that 1% back to the pension company as commission too (I say, jolly good, eh?). You end up investing in poorly performing markets such as Japan, UK, EU, emerging markets, etc. etc. Typically 50-100 different funds. Also many of these funds actually invest in the same stocks.

So the pension companies have invested across the whole world market anyway, but, of course, each of these funds have hidden the 2-4% fund charges from you as well as them paying the pension company commission (though it may not be called that!). Basically, your pension may just keep up with inflation but the wonderful effect of compound interest for 20 years helps to mask this!

In the 'old days' you could only set up your own portfolio if you had your own broker on the phone, wore braces and were prepared to spend weeks buying and selling stocks, etc. But these days we have the INTERNET and we have ETFs. These two things make it so simple and will save you tens of thousands of pounds (and probably much more).

So is it really risky to invest in something like a World/Global Index tracker ETF like SWDA (there are many others), which have performed much better?

Here is a 15 yr chart comparing the FTSE 100 (170% gain) with SWDA (top companies across the world - 400% gain!). Note that this does not take into account the 2-4% hidden charges of your pension company which will dramatically reduce the FTSE gain!

15 years - SWDA (Orange) vs FTSE 100 (Blue)

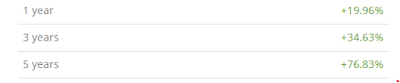

SWDA returns

So in last 5 years, SWDA averaged 76/5 = 15%. Now compare this with your current pension fund performance which is probably less than 6% (net of charges)!

P.S. You can see the effect of Covid in 2020 but the world market recovered much quicker that the FTSE!

So, from the graph, both the FTSE and SWDA had similar performance gain to start with. There were dips and recoveries in both. The only difference is that from 2014, SWDA starts to outperform the FTSE and makes twice as much! If you managed your own pension, would you have put a lot of your money on the FTSE? Why are pension companies still putting a large proportion into FTSE funds? Are they lazy or out of touch but just take the commission anyway? Are they really acting in your interest?

If you are really afraid of losing everything in a stock market crash, then buy FTSE as well as SWDA and also keep a proportion in bonds and cash and gold (e.g. gold SGLN ETF). Unlike a standard pension scheme, you can change it around at any time with no capital gains tax penalty.

What companies are inside your pension portfolio?

If possible, as well as the performance of your personal pension, ask for a list of the funds in your pension portfolio. If that list contains lots of UK FTSE or EU funds as well as dozens of other funds, ask yourself why are they heavily investing your money in those markets when the sensible investors are mainly investing in World, US and Tech stocks? Do they really care about you and your money or are they just playing it ultra safe and covering their own a$$es by keeping a lot of your pension in low-rate safe bonds for 30 years so they cannot be blamed if there is a terrible crash but still take their fund and management fees?

What is an ETF?

An ETF is an 'Exchange Traded Fund' - it is a basket of companies all in one wrapper. When you invest in an ETF, you are (typically) investing in all the companies within that ETF. You own those shares - they are yours. If your broker company went bust, you would still own those shares.

Some ETFs are actively managed (the companies are selected based on specific criteria) or passively managed (e.g. they just buy the top 100 companies - whatever they currently happen to be).

Passive tracker ETFs are normally safer, perform better and are cheaper than active ETFs (for active ETFs - it just depends on how good the picker is that day and how playful he/she wants to be with your money!).

ETFs do have a hidden annual charge, but this charge is included in the ETF price, so you don't actually need to pay it separately or worry about it. Index tracker ETFs tend to have lower charges (e.g. typ. 0.1-0.2%). Compare this with a pension companies charge of 1%+ (10 times higher) not even counting the hidden TER costs within the funds they are buying with your money!

What is an Index ETF?

An index ETF is designed specifically to replicate a benchmark index such as the Dow Jones Industrial Average, Nasdaq 100, FTSE 100, FTSE 250 or S&P 500, etc.

What is a Tracker ETF?

These funds are described as ‘passive’ investments as they simply aim to replicate the performance of a benchmark or market index.

What is an Index Tracker ETF?

Index tracker funds – also known as ‘index’, ‘tracker’, or ‘passive’ funds – are a type of ‘pooled’ or ‘collective’ investment scheme.

A pooled arrangement aggregates sums of money from lots of different people into one large fund allowing it to be managed on their behalf by a professional investment management firm.

Index trackers aim to replicate the performance of a certain stock market index, such as the UK’s FTSE 100, or the S&P 500 in the US.

As an investor in a tracker fund, you can only (at best) expect to mimic the performance of a particular index. It’s important to remember that the money you invest in a tracker will, over time, follow the movements of an index – down as well as up.

Index tracking is in contrast to so-called ‘actively managed’ funds run by professionals who pick specific stocks in order to beat an underlying index. Pension companies tend to pick dozens of these sorts of high-cost funds. It helps pay for their Ferraris and Porsches.

Index tracker funds come in a variety of guises. As well as those that track particular stock market indices, products may also focus solely on a specific industry or sector (such as technology or healthcare), countries or particular investing styles (such as ESG).

How do index trackers work?

When you put money into an index tracker fund, the cash is used to invest in all the companies that make up a particular index. This provides the investors with a more diverse portfolio compared with buying, say, just a concentrated handful of stocks.

Index tracker funds aim to mirror a specific index as closely as possible and they try to do this in one of two ways.

The first method is by a process known as ‘full replication’, which essentially means buying all the components of a particular index. For example, in the case of a FTSE 100 tracker, a tracker fund will buy shares in all 100 companies within the FTSE 100 index in proportion to the size of each company as it appears within the index.

The second process is called ‘partial replication’. Rather than buy all the shares in an index, tracker funds in this camp invest in a representative sample of companies that feature on a particular index e.g. the 50 top quality companies only.

Index funds, ETFs and stocks: what’s the difference?

Stocks are units of ownership in an individual company, rather than a portfolio of assets as with funds and ETFs, and are traded using live prices.

Index funds and ETFs share similar characteristics as they are both ‘passively-managed’ and aim to track or replicate an index. However, their different legal structures affect the way in which they’re bought and sold.

OK - so what should I do?

Well, everyone's circumstances are different. I cannot tell you the 'right' thing to do because I don't know your age or circumstances and I am not qualified any way.

If you are below 50 years of age, you definitely should be researching your current pension scheme and (if in UK) and you have no other options then think seriously about switching it to a self-investment SIPP (ask if you can invest in the SWDA ETF as a test - if they say no, then you will have to transfer your pension to someone else). Always take unbiased independent advice before switching your pension though!

Most investors agree that in the current economic climate, it is stupid for a (18-50) person to invest heavily in bonds and UK/EU stocks (which is exactly what pension companies do with your money!).

If you are over 50, you may need to think more carefully. You could invest in an ETF and the whole world stock market could plummet by 50%. Many pensions hold a certain proportion of your pension pot in bonds. These are thought to be relatively safe from market collapse. For instance, you could have 40% of your pension in bonds and 60% in ETFs. In this case you might like to consider a Vanguard (YT video) 'LifeStrategy' fund which are specifically designed to protect you from such an occurrence (when you start drawing on your pension pot on retirement). The best Vanguard funds can tailor the portfolio so that it is less volatile as you near retirement age (e.g. the 'Target Retirement 2045' fund, etc. - a great idea for the cautious and cheap to run at 0.2%ish, but they still tend to invest more heavily in UK FTSE so the gains are poor but still they much better than most other pension company funds as long as you can start it at least 5 years before retirement).

The Vanguard 'LifeStrategy Retire at 2045' fund performance. As 2045 approaches, the gain will reduced as more of your money is invested into low-risk bonds. This is a much easier and better pension than a standard pension fund which typically returns 4%-6% (but you could do better yourself - Vanguard 9% vs SWDA 15%).

You could easily replicate this yourself however using just say SWDA (global ETF) and CSH2 (or a bond ETF).

30 Years to retirement: 100% SWDA

10 Years to retirement: 80% SWDA + 20% CSH2

5 Years to retirement: 60% SWDA + 40% CSH2

Retirement: adjust ratio (typically you will want to draw 4% a year for a sustainable pension, so it depends on the amount you need and how long it needs to last).

Of course, you could also invest in other ETFs as well as SWDA to get an even better return or provide diversification.

But what should I invest in?

It depends on your attitude to risk. Tech ETFs like IITU have performed amazingly (50% last year!) but they could crash to 30% of their value (but very unlikely unless Microsoft, Nvidia, Apple, Netflix, Amazon, etc. all went bust!). Even if tech stocks do plummet, they will usually recover in 1-2 years and then outperform most other funds.

Some ETFs allow you to hold safe bonds/money market cash (e.g. CSH2), so you could hold say 40% of you pension in CSH2 at a steady interest rate, but recent history has shown that not even bonds are safe from the affects of the stock market. Instead of holding bonds, some online brokers allow you to keep a portion as cash and will pay you a reasonable interest rate.

There are many YouTube videos on investing in ETFs, so go and have a look - see below!

You can research most ETFs at www.justetf.com. If you (i.e. your ISP) are located in the UK, the website will automatically only list for you the ETFs that you can purchase in the UK (GBP) on the justetf site.

Here are some for you to look at - you can, of course, have a mixture of these and in any proportion you wish (the more specialised ones are more risky but offer higher returns):

ETFs (available in UK)

SWDA - world index tracker - used as benchmark standard

CSPX. - S&P 500 recommended by Warren Buffet

IITU - S&P 500 Technology stocks - is there about to be a correction soon?

IUCM - S&P 500 Communication stocks

EQQQ - NASDAQ 100 - pays dividends (or XNAQ which accumulates dividends)

VUKG - Vanguard FTSE

XDEV - World Value companies (Cisco, Qualcom, Toyota, Intel, IBM, etc.)

EMSM - Emerging markets small caps

CYSE - Cyber Security companies

SGLN - Tracks Physical Gold price

JPHG - Japan Nikeii

IQSA - Global ESG

Many others are available - these are just a sample. You can pick a sector (metals, property, commodities, etc.) and/or a geographical location (USA, Japan, Far East, EU non-UK, etc.).

To start, I would just invest in SWDA and then branch out later as you do more research.

You could have 80% in SWDA and 20% in IITU or other ETFs for instance, and if the Tech bubble bursts, after viewing the data on justetf.com, you can sell some or all IITU and buy XDEV instead or just do nothing and wait for it to recover (which is usually best). You are in control!

How do I manage the ETFs in my pension portfolio over time?

I suggest you look at the performance of your ETFs at least once a year. Usually you can ignore minor downward blips of up to -20% (assuming benchmark ETFs like world market, USA, EU, UK, etc, and not a mining or oil ETF), these blips are usually temporary and will eventually recover (though it may take up to a year).

Every year or 6 months you should ask yourself the question, 'does this portfolio look OK for me for the next year'? This is especially important if you are drawing down on your pension (e.g. retired). A volatile portfolio can be badly dented if you make withdrawals during a recession because you are withdrawing money whilst the total value is depressed. This is why you should consider holding less volatile ETFs (which may have less gain but also will lose less) if you are retired and drawing funds from it. The FTSE will track the UK economy and so will your pension pot. You should get advice from an IFA before drawing on your pension (typ. charge £500) - they can save you thousands of pounds and so they are well worth it!

P.S. Unless you know more than everyone else and are prepared to lose heavily, never invest in individual companies! I always recommend index tracker ETFs.

IMPORTANT: I am not a financial advisor and you should do your own research. The intention of this article is to make you aware of the many thousands of pounds/dollars you may be giving away and how upset you may be when you do finally retire and it is too late to do anything about it except kick yourself!

No comments:

Post a Comment